A US-side reading of the May 2026 AVK / CompositesWorld market report — and what it implies for inspection capacity, certification, workforce development, and trends in aerospace composite inspection.

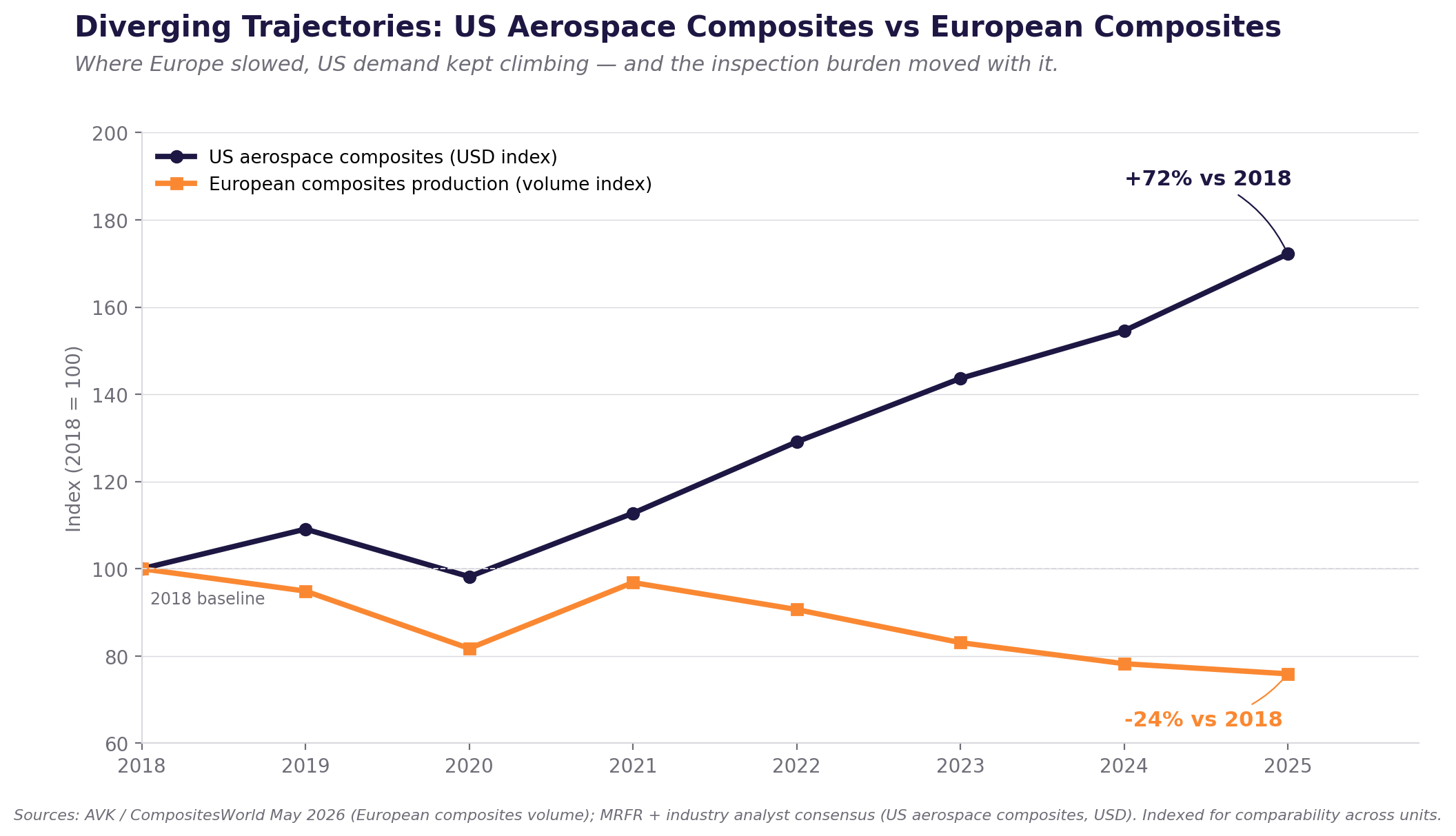

The AVK’s annual composites market report, summarized in CompositesWorld this May, leads with a headline most US readers would skim past: European composites production fell about 3% in 2025, ending the year at 2,281 kilotons against 2,351 the year before. That’s roughly a 70-kiloton drop, mostly automotive-driven.

The other half of the report is what matters here.

Global composites demand is still climbing — JEC estimates the worldwide market at somewhere between 13.3 and 15.9 million tons, growing about 1% in 2025 — and Europe’s share is falling. From around 17% in the low-case estimate down to 14% in the high case. The volume Europe doesn’t produce gets sourced somewhere else. Increasingly, that somewhere is the Americas and Asia.

That shift is what makes the report worth reading from Ogden.

The US numbers driving aerospace NDT demand

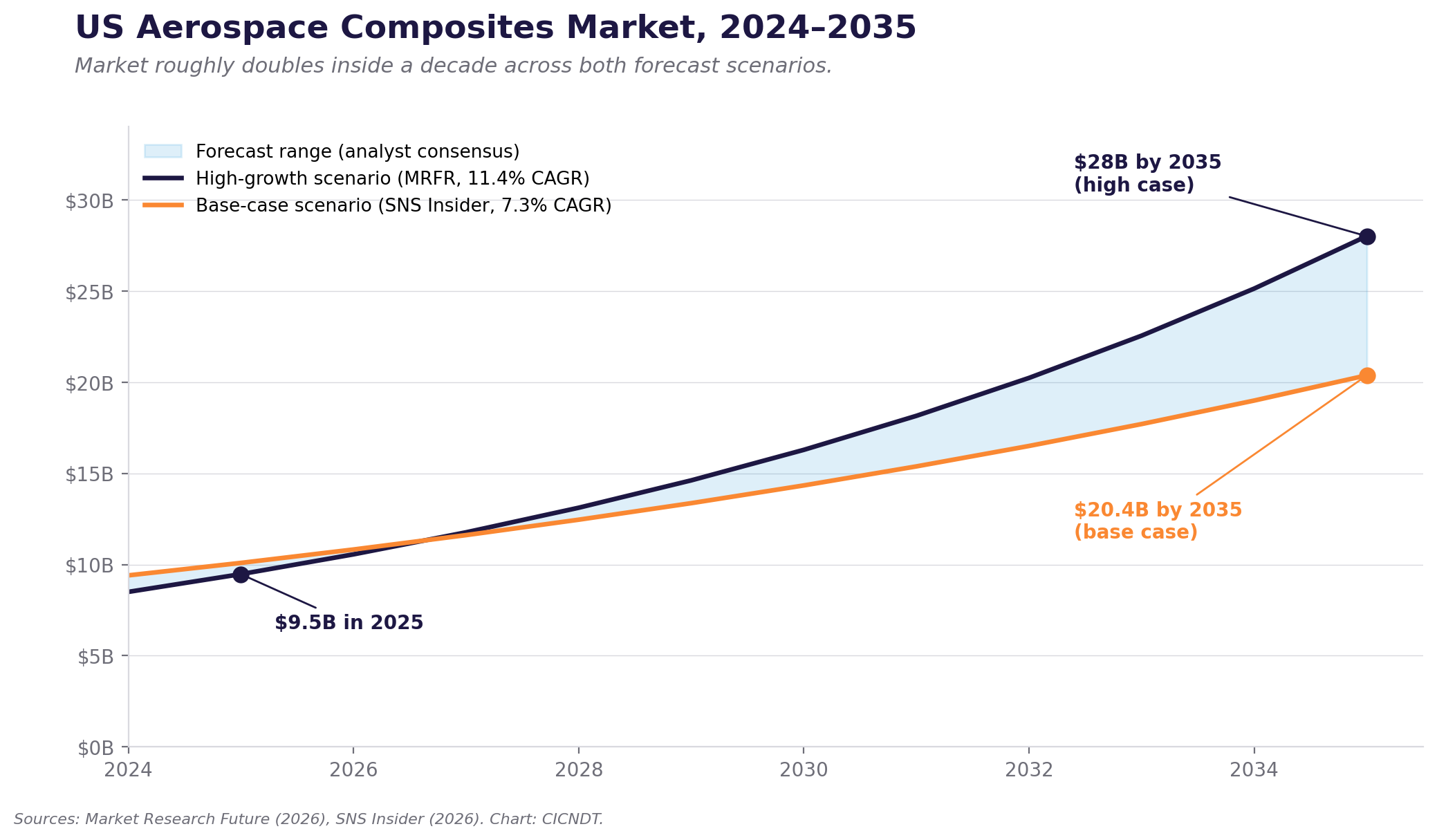

US aerospace composites stood at roughly $9.5 billion in 2025. Market Research Future projects $28 billion by 2035 at an 11.4% CAGR; SNS Insider models a more conservative path to about $20 billion at 7.3%. Either way, the market roughly doubles inside a decade. North America already accounts for around 30% of global aerospace composites.

The underlying drivers aren’t hypothetical. Lockheed plans to deliver around 190 F-35 airframes in 2025, up from 156. Modern combat aircraft run 30 to 50 percent composite by weight. The Navy’s 30-year shipbuilding plan calls for advanced composite materials in roughly 35% of new vessels, up from about 22% a decade ago, and NAVSEA has earmarked around $1.2 billion for composite integration on those programs. Wind, eVTOL, hypersonics, satellite structures, and high-pressure tank applications all stack additional demand on top. NASA’s HiCAM program is pushing thermoplastic welding qualification into production-grade use.

If you read only the AVK summary, the impression is that composites are slowing down. If you read it next to the US Navy’s shipbuilding plan and Lockheed’s F-35 delivery cadence, the impression is the opposite. Both are true. The work is just moving.

Why this matters for composite NDT

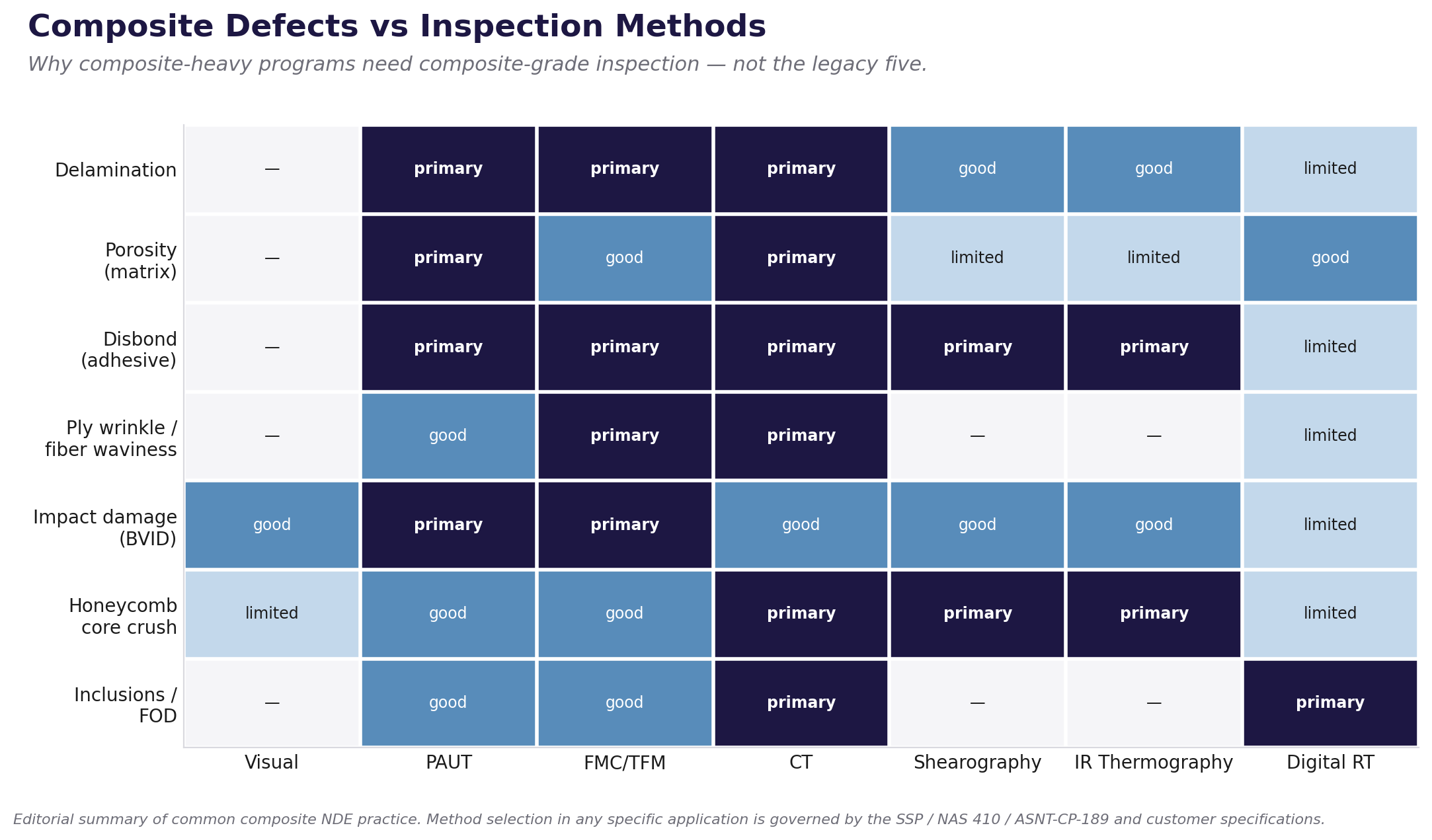

Composites don’t fail the way metals fail. They delaminate. They develop porosity in the resin matrix. Bondlines weaken before they break. Ply wrinkles concentrate stress invisibly. Honeycomb sandwich panels crush in core regions a visual inspector can’t see. None of those announce themselves to a flashlight inspection.

That’s why the inspection mix on composite parts looks nothing like the inspection mix on aluminum airframes. It runs heavily toward phased array ultrasonics (PAUT), increasingly with FMC/TFM imaging for higher resolution on complex layups; computed tomography for bonded joints, internal geometry, and certification-quality void mapping; shearography and infrared thermography for honeycomb and bonded structures, where back-side air gaps are the defect of interest; and digital radiography for fastener-heavy assemblies.

CT in particular is becoming the certification-quality method for critical composite parts. Mordor Intelligence projects CT growth in aerospace NDT at about 10.5% CAGR through 2031, the fastest of any modality. Olympus put $40 million into portable CT specifically for eVTOL airframe inspection in May 2025. In July, the FAA released Advisory Circular AC 43.13-1C, which laid out certification pathways for AI-enabled NDT systems. The regulatory infrastructure is catching up to where the technology already is.

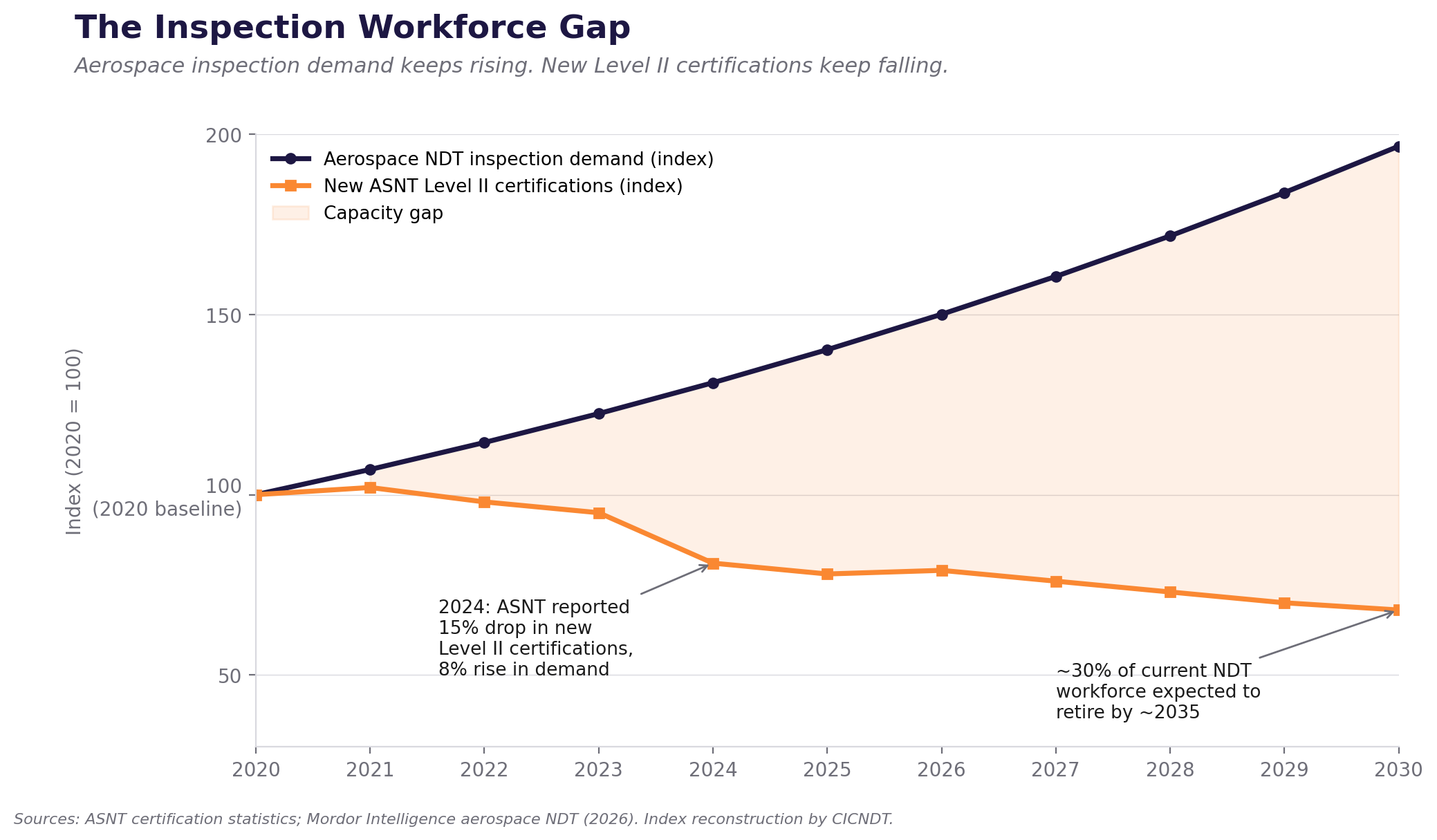

The composite inspection workforce nobody’s solving fast enough

The inspection industry has a workforce problem.

The American Society for Nondestructive Testing reported that new Level II certifications in the US dropped 15% in 2024 — the same year industry demand for inspection rose 8%. ASNT also estimates the global shortfall in Level III talent at around 40%. Roughly 30% of the current US NDT workforce is expected to retire over the next decade. The average US NDT technician is over 40 years old.

That math doesn’t reconcile. If aerospace composites doubles by 2035 and certifications keep falling, someone has to inspect the parts. The current answer in most shops is overtime, contract Level IIIs flying in to oversee critical jobs, and a quiet acceptance that backlogs keep growing. None of those scale.

ASNT updated SNT-TC-1A in April 2025 to formally recognize digital and AI-assisted methods — PAUT with FMC/TFM, AI-classified inspection, full-matrix capture — inside the competency expectations. That’s the right move. But certification rules update faster than people do. You don’t fix a thirty-percent retirement wave with a document change.

What aerospace composite inspection at CICNDT looks like

The International Committee for Certification in Nondestructive Testing exists to certify inspectors against a consistent international standard, not a patchwork of company-specific programs. That matters more now than it did ten years ago. A composite part fabricated in Huntsville, finish-cured in Ogden, and inspected by a contractor in Greenville doesn’t care which company’s training program the inspector graduated from. It cares whether the inspector can find the defect, and whether the certification on file actually proves they can.

CICNDT is the core of the AIMM Center in Ogden, sharing the facility with Omni NDE on the applied technical side. That setup is deliberate. Standards developed in isolation from the working methods drift, and methods developed without certification scaffolding don’t propagate. Putting certification, training, and live inspection work under one roof keeps both sides honest.

The certification side has to map to the methods composites actually need now — PAUT, CT, shearography, infrared thermography, and increasingly AI-classified analysis — not just the legacy five. The training side has to produce technicians who are useful on day one. The CICNDT Academy is built around modular, instructor-led delivery with real practical exercises, configured either at the customer’s site or at the Ogden facility, a few miles from Hill AFB. The applied side, where Omni NDE runs the inspection and methods work, gives the certification and training programs direct visibility into how those methods perform on real composite hardware — and gives industry partners a single point of contact for the inspection-to-lifecycle data integration composite programs increasingly require.

None of that closes the workforce gap by itself. But the gap doesn’t close without infrastructure that’s specifically scoped to it. Industry-wide retirements aren’t going to slow down. Composite tonnage going through US shops isn’t going to slow down. Programs that don’t intersect those two trendlines aren’t going to matter much.

The view from June 2026

The Gardner Composites Fabricating Index registered 52.1 in March — above the 50 threshold, expanding. The Future Business Index sat at 67, well into expansion territory. Indices aren’t predictions, but they’re a useful read on what operators are seeing in their order books. The work is coming. The fleet is composite-intensive. The Department of Defense’s proposed $1.5 trillion budget includes substantial composite-bearing platforms in production or accelerated procurement.

The question for the inspection side of the supply chain isn’t whether the work is there.

It’s whether enough certified inspectors will be.

That’s the work in front of us.

Sources

- Mathes, V. “Europe’s Composites Market Trajectory.” CompositesWorld, May 2026 (based on AVK Federation of Reinforced Plastics annual market analysis).

- Shirk, M. “Gardner Business Index — Composites Fabricating.” CompositesWorld, May 2026.

- Mordor Intelligence (2026): “Aerospace Composites Market” and “NDT in Aerospace & Defense Market.”

- Market Research Future (2026): “US Aerospace Composites Market” 2025–2035 outlook.

- SNS Insider (2026): “Aerospace Composites Market” 2026–2035.

- Fortune Business Insights (2026): “Non-Destructive Testing (NDT) Market.”

- American Society for Nondestructive Testing — SNT-TC-1A revision (April 2025) and certification statistics.

- Federal Aviation Administration, Advisory Circular AC 43.13-1C (July 2025).

- Department of the Navy, 30-Year Shipbuilding Plan.

CICNDT — Composite Inspection and Non-Destructive Testing. 690 W 1100 S Suite 7, Ogden, UT 84404 · (801) 436-6512 · cicndt.com